The Single Strategy To Use For Paul B Insurance

Related Subjects One reason insurance coverage problems can be so confounding is that the health care market is regularly altering as well as the coverage prepares supplied by insurers are difficult to classify. In various other words, the lines between HMOs, PPOs, POSs and also various other kinds of coverage are frequently blurry. Still, understanding the make-up of numerous strategy kinds will certainly be useful in assessing your options.

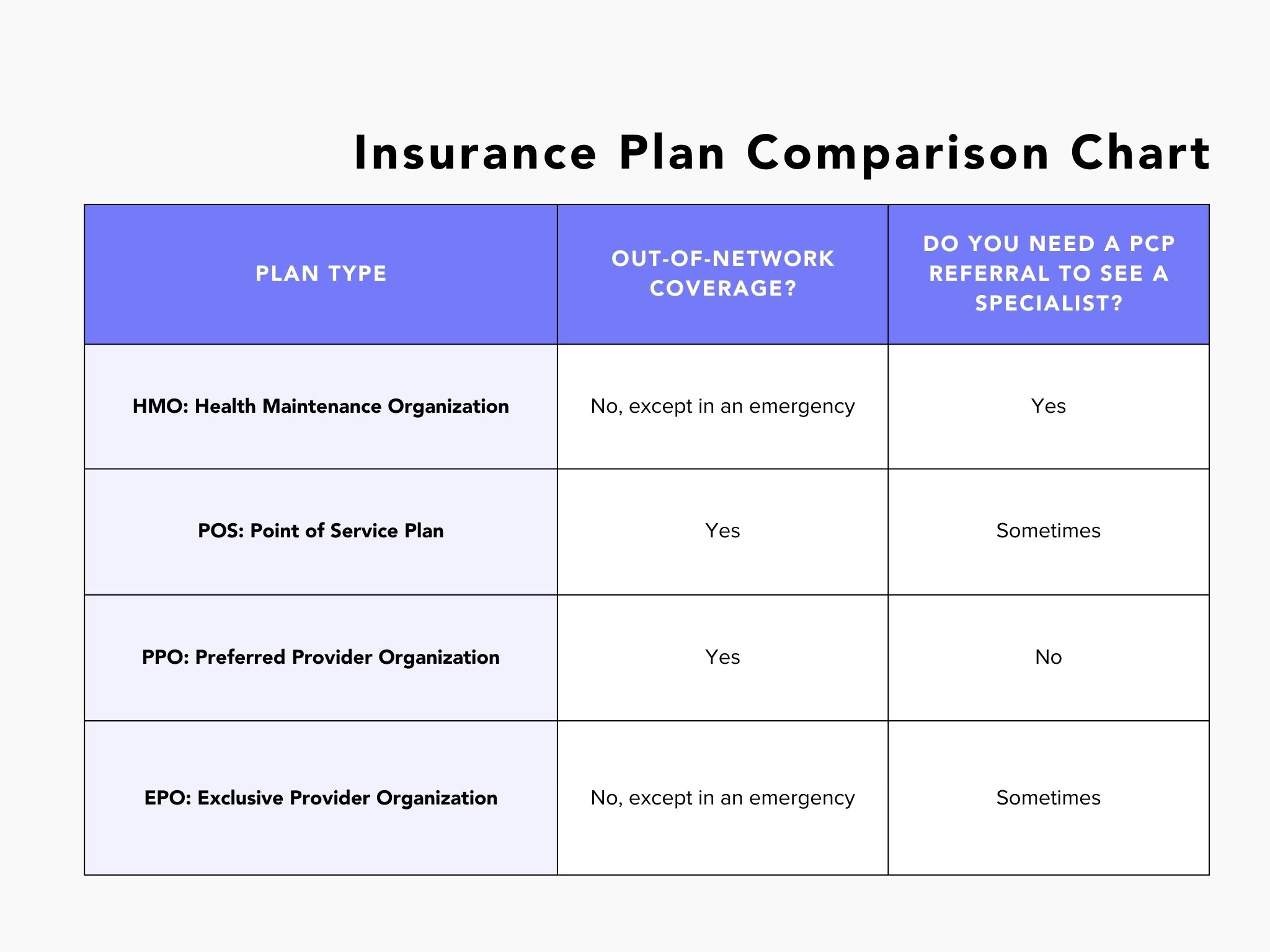

PPOs generally use a larger option of carriers than HMOs. Costs might be similar to or somewhat more than HMOs, as well as out-of-pocket prices are usually greater and also a lot more difficult than those for HMOs. PPOs enable participants to venture out of the carrier network at their discretion and do not call for a recommendation from a health care doctor.

Once the insurance deductible amount is reached, added health and wellness expenditures are covered according to the provisions of the medical insurance plan. As an example, an employee could then be accountable for 10% of the expenses for treatment obtained from a PPO network company. Down payments made to an HSA are tax-free to the employer and also staff member, and also money not spent at the end of the year may be surrendered to spend for future medical costs.

Paul B Insurance Fundamentals Explained

(Employer payments have to coincide for all employees.) Employees would be in charge of the first $5,000 in medical expenses, but they would each have $3,000 in their individual HSA to pay for clinical costs (and would have much more if they, also, added to the HSA). If employees or their family members tire their $3,000 HSA allocation, they would pay the next $2,000 out of pocket, whereupon the insurance coverage would start to pay.

There is no restriction on the quantity of money an employer can add to worker accounts, however, the accounts might not be funded via staff member wage deferments under a lunchroom strategy. In addition, companies are not permitted to refund any type of part of the balance to staff members.

Do you understand when the most wonderful time of the year is? The magical time of year when you obtain to contrast health insurance policy prepares to see which one is ideal for you! Okay, you got us.

The Best Guide To Paul B Insurance

But when it's time to pick, it is very important to recognize what each plan covers, just how much it sets you back, and also where you can use it, right? This stuff can really feel complex, but it's less complicated than it appears. We assembled some functional learning steps to help you feel great about your options.

(See what we did there?) Emergency care is frequently the exemption to the guideline. These plans are the most popular for people who obtain their medical insurance via work, with 47% of protected employees enrolled in a PPO.2 Pro: The Majority Of PPOs have a suitable choice of service providers to pick from in your location.

Con: Higher premiums make PPOs extra expensive than other sorts of strategies like HMOs. A health and wellness maintenance organization is a health and wellness insurance policy strategy that normally just covers treatment from doctors who benefit (or contract with) that specific plan.3 Unless there's an emergency situation, your plan will certainly not pay for out-of-network treatment.

The 8-Second Trick For Paul B Insurance

More like Michael Phelps. It's good to know that strategies in every classification offer some types of complimentary preventative treatment, as well as some deal cost-free or discounted medical care solutions before you fulfill your deductible.

Bronze strategies have the most affordable regular monthly costs however the highest out-of-pocket costs. As you function your way up with the Silver, Gold and also Platinum groups, you pay extra in premiums, however less in deductibles as well as coinsurance. However as we stated previously, the additional costs in the Silver group can be lessened if you get approved for the cost-sharing reductions.

Reductions can lower your out-of-pocket medical care costs a lot, so get with among our Recommended Regional Carriers (ELPs) who can help you discover out what you might be eligible for. The table below programs the portion that the insurance company paysand what you payfor covered expenses after you fulfill your deductible in each strategy category.

Some Of Paul B Insurance

Various other prices, frequently called "out-of-pocket" costs, can add up swiftly. Things like your insurance deductible, your copay, your coinsurance quantity and also your out-of-pocket maximum can have a huge impact on the total price.

When picking your wellness insurance coverage plan, don't forget health care Visit Website cost-sharing programs. These job rather a you can try these out lot like the other medical insurance programs we explained currently, but technically they're not a article form of insurance policy. Permit us to describe. Wellness cost-sharing programs still have month-to-month costs you pay as well as specified coverage terms.

If you're trying the do it yourself path as well as have any type of remaining inquiries about medical insurance strategies, the experts are the ones to ask. And also they'll do even more than simply address your questionsthey'll likewise discover you the very best price! Or maybe you would certainly such as a means to incorporate getting fantastic healthcare coverage with the chance to assist others in a time of demand.

The 2-Minute Rule for Paul B Insurance

Our trusted partner Christian Health care Ministries (CHM) can help you find out your alternatives. CHM assists households share healthcare costs like clinical tests, pregnancy, a hospital stay as well as surgery. Hundreds of individuals in all 50 states have actually made use of CHM to cover their health care requires. Plus, they're a Ramsey, Trusted companion, so you recognize they'll cover the medical costs they're meant to and honor your insurance coverage.

Trick Question 2 One of the points healthcare reform has done in the united state (under the Affordable Care Act) is to present more standardization to insurance policy strategy advantages. Prior to such standardization, the advantages offered different significantly from plan to plan. As an example, some strategies covered prescriptions, others did not.